Discover the pros and cons of investing in structured notes

The market potential for structured notes has achieved steady growth over the years, with the flexible nature of structured notes evolving to meet changing economic needs. In an uncertain market, structured notes offer products that include capital protection and higher than average returns for structured investments.

In fact, PwC’s predictions are published in the 2020 report ‘Asset and wealth management revolution: embracing exponential change’, and find as investors seek to reduce volatility, alternative assets specifically real assets, private equity and private debt, are set to double in size to the tune of $21 trillion (USD) in the next eight years.1

Another notable estimate from PwC is that by 2025, assets under management will reach the value of $145 trillion (USD) from an industry that was worth $84.9 trillion (USD) in 2016.2 This shows that structured notes will have a role to play in investors’ portfolios in the years to come.

Part of the benefits that arise from structured notes is the way that they can be diversified in terms of growth or income notes. Mainly as these investment products pay a higher return at the cost of moderate risk to the investor’s capital while offering a level of capital protection and some stock market exposure.3

Structured notes can provide the following:4

- Growth notes – with autocalls that centre on good growth of the underlying asset and may return capital before the end of their fixed term.

- Income notes – with a focus on regular high-level income (coupons) across a fixed term.

For investors that are looking for medium- to long-term capital growth with a lower or moderate level of risk; structured notes meet the requirements of downside protection (lesser risk to capital loss), enhanced participation, a regular coupon interest payment or a payout upon maturity if specific market conditions are present or met.5

For a better distinction on the difference between growth or income structured notes, we have two examples from our partner Cashbox Global on Wealth Migrate’s FinTech platform.

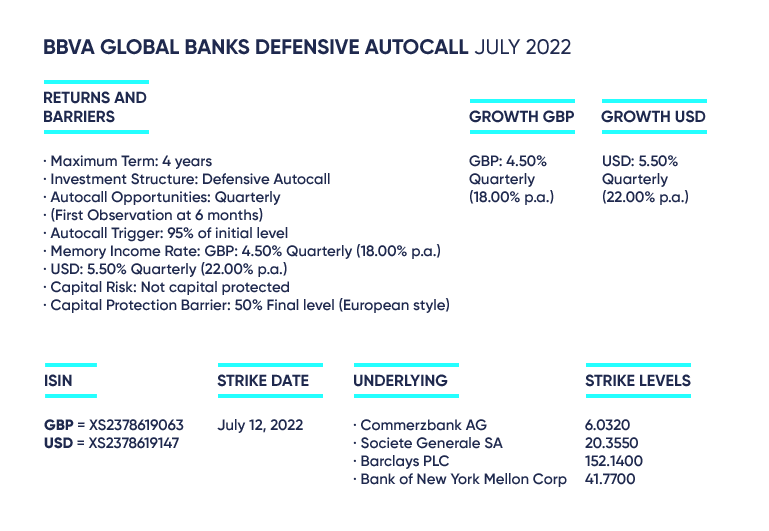

Example one: growth structured note

Important details to be aware of

The underlying assets are a reference basket for the coupon (interest payment) that is accrued. Investors do not own actual shares in the companies, rather the prices of the underlying assets determine whether the autocall option will be reached.

One of the features that makes this growth note remarkable is that it has a memory feature where the coupons accrue and roll up until the structured note autocalls, and then all the accumulated coupons will then be paid out.

Since this is a growth-orientated structured note the coupons are not paid out quarterly, and accrual of the coupons will stop once the investment reaches the auto call level and matures early or until it reaches maturity at the end of the four-year period. If the structured note’s underlying assets perform well and it reaches early maturity, investors could still receive coupons as the minimum payment period is six months (subject to an autocall event).

This is a hypothetical situation to more simply explain how this works

If the underlying reference basket is simply labelled A, B, C, and D and the value of the underlying assets is $100 (USD) when an investor accepts the terms of the structured note and invests.

- An autocall trigger will occur if all the levels of the underlying assets are at or above 95%. For instance, if A, B, C, and D reach $195 (USD).

If an autocall is triggered, full capital along with the accumulated coupons for each quarterly observation period that has elapsed will be repaid, and the investment will end. - There is, however, capital protection at 50% of the initial levels (A, B, C, and D’s price), this only applies at the final observation date if the note did not autocall.

At the final observation date, if all underlying assets are at or above 50% of their initial levels, then full capital is returned. In the instance that A, B, C, and D only reach $50 (USD) at the end of four years, no coupons will be payable, but investors are paid back all their capital. - In a worst-case scenario, where the worst performing underlying asset devalues to 40% of its initial level.

No coupons are payable and only 40% of the capital will be returned. This scenario is similar to a direct stock market investment, where investors’ exposure to the stock is executed at the current ruling price.

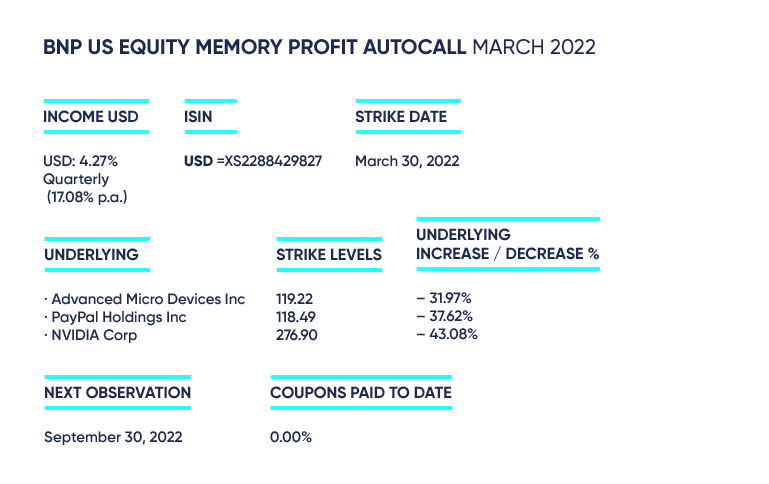

Example two: income structured note

Important details to be aware of

The underlying assets are a reference basket for the coupon (interest payment) that is accrued. Investors do not own actual shares in the companies, rather the prices of the underlying assets determine whether the autocall option will be reached.

The quarterly coupon distributions are subject to the performance of the underlying assets, measured at each profit observation date. The memory feature ensures that any previously unpaid profit, should the profit payment not be triggered at an observation date, will be caught up when the next profit trigger is activated.

The first autocall opportunity will only take place after 12 months and effectively locks in a minimum distribution payment over that period due to investors, given that the profit trigger is met. This structured note has a maximum four-year investment term – if early maturity does not occur – the investment will continue to the final observation date.

This is a hypothetical situation to more simply explain how this works

If the underlying reference basket is simply labelled A, B, and C, and the value of the underlying assets is $100 (USD) when an investor accepts the terms of the structured note and invests.

- A profit trigger will occur at or above 75% of the closing levels of the underlying assets. For instance, if A, B, and C reach $175 (USD).

The profit (interest payments) will be paid on any of the quarterly observation dates, including the final observation date if the closing levels of all the underlying assets are at or above 75% of their initial levels. Plus, any previously missed profit payments due to the memory profit feature. - An autocall trigger will occur if all the levels of the underlying assets are at or above 100%. For instance, if A, B, and C reach $200 (USD).

This investment will autocall and mature early if the levels of all underlying assets are equal to or above the autocall trigger on any quarterly observation date. - There is, however, capital protection at 65% of the initial levels (A, B, and C’s price), this only applies at the final observation date if the note did not autocall.

At the final observation date, if all underlying assets are at or above 65% of their initial levels, then full capital is returned. In the instance that A, B, C, and D only reach $65 (USD) at the end of four years, no profit will be payable, but investors are paid back all their capital. - In a worst-case scenario, where the worst performing underlying asset devalues to 40% of its initial level.

No profit is payable and only 40% of the capital will be returned. This scenario is similar to a direct stock market investment, where investors’ exposure to the stock is executed at the current ruling price.

As part of an ongoing educational series, our next article will explore the highlights of digitalisation’s impact on structured notes. Find out how the structured note has evolved under the influence of tech

1 Alexander, O., Benjamin, B., Holly, T., et al. (2020). ‘Asset and wealth management revolution: embracing exponential change. Retrieved from PwC.

2 Alexander, O., Benjamin, B., Holly, T., et al. (2020). ‘Asset and wealth management revolution: embracing exponential change. Retrieved from PwC.

3 Cashbox Global. (April 2022). ‘Types of structured notes’. Retrieved from LinkedIn.

4 Cashbox Global. (April 2022). ‘Types of structured notes’. Retrieved from LinkedIn.

5 Bredenkamp, B. (November 2021). ‘Have you considered investing in structured products?’. Retrieved from Moneyweb.